Thursday, September 30, 2010

Quarterly Economic figures...

...Productivity and Gross Domestic Purchases being the notables in the latest Data from the U.S. Treasury.

Not for sovereigns...

From this article in Reuters.

"You can find a quick fix -- borrow some money and make this structural problem even worse, and then the next government comes in and you will have a debt crisis... there could be short-sightedness in borrowing," she said.

The principles will guide both borrowers and lenders, as a loan is a two-way contract and those providing the money must do their due diligence to ensure it can be paid and used correctly.

Who provides "money" to whom when sovereigns are concerned and covertibility to a commodity is not an issue? This conceptualization is misguided as sovereign states do not need to "get" money in order to spend the currency they themselves issue.

Iceland's president, Olafur Ragnar Grimsson, discussed his country's debt crisis at the Xiamen meeting and said that principles to avoid reckless lending and borrowing should be encouraged, UNCTAD said.

The project, funded in part by the Norwegian government, aims to create rules to prevent irresponsible lending to states and enable courts to test the legitimacy of debt when disputes arise.

It is realistic to finish revising the principles next year even though a lot of technical work remains to be done, and not all governments and institutions fully understand the detail of what has been proposed so far, Li said.

"You can find a quick fix -- borrow some money and make this structural problem even worse, and then the next government comes in and you will have a debt crisis... there could be short-sightedness in borrowing," she said.

The principles will guide both borrowers and lenders, as a loan is a two-way contract and those providing the money must do their due diligence to ensure it can be paid and used correctly.

Who provides "money" to whom when sovereigns are concerned and covertibility to a commodity is not an issue? This conceptualization is misguided as sovereign states do not need to "get" money in order to spend the currency they themselves issue.

Iceland's president, Olafur Ragnar Grimsson, discussed his country's debt crisis at the Xiamen meeting and said that principles to avoid reckless lending and borrowing should be encouraged, UNCTAD said.

The project, funded in part by the Norwegian government, aims to create rules to prevent irresponsible lending to states and enable courts to test the legitimacy of debt when disputes arise.

It is realistic to finish revising the principles next year even though a lot of technical work remains to be done, and not all governments and institutions fully understand the detail of what has been proposed so far, Li said.

Pot. Kettle. Black.

Interesting opinion regarding release of information and calls of transparancy...

The International Monetary Fund criticized Wednesday the abuse of sovereign debt ratings, warning that credit rating agencies may wield undue influence with investors.

"Sovereigns should do more to provide relevant and timely information to CRAs (credit rating agencies) and other market participants to enable them to conduct their own independent credit analysis," the IMF said in a synopsis of a report entitled "The Uses and Abuses of Sovereign Credit Ratings."

The report, a chapter in the biannual Global Financial Stability Report due to be released in full next week, examines the roles of the top three CRAs: Fitch, Moody's and Standard & Poor's.

A key focus of the study was to determine whether they rate sovereign debt accurately.

The problem was a key factor in the Greek debt crisis earlier in the year, as agency downgrades helped to accelerate the country's descent to the brink of default.

Once a credit rating is lowered to a certain level -- "Ba1" and less for Moody's, "BB+" and less at rival S&P, for instance -- certain investors are required to sell a bond deemed "speculative," which automatically lowers its value.

The International Monetary Fund criticized Wednesday the abuse of sovereign debt ratings, warning that credit rating agencies may wield undue influence with investors.

"Sovereigns should do more to provide relevant and timely information to CRAs (credit rating agencies) and other market participants to enable them to conduct their own independent credit analysis," the IMF said in a synopsis of a report entitled "The Uses and Abuses of Sovereign Credit Ratings."

The report, a chapter in the biannual Global Financial Stability Report due to be released in full next week, examines the roles of the top three CRAs: Fitch, Moody's and Standard & Poor's.

A key focus of the study was to determine whether they rate sovereign debt accurately.

The problem was a key factor in the Greek debt crisis earlier in the year, as agency downgrades helped to accelerate the country's descent to the brink of default.

Once a credit rating is lowered to a certain level -- "Ba1" and less for Moody's, "BB+" and less at rival S&P, for instance -- certain investors are required to sell a bond deemed "speculative," which automatically lowers its value.

Wednesday, September 29, 2010

Currency wars...

...a continuing series. This in light of China's "commitment" for "flexible" exchange rates.

(From FT's Alphaville)

Within a single week 25 nations have deliberately slashed the values

of their currencies. Nothing quite comparable with this has ever

happened before in the history of the world. This world monetary

earthquake will carry many lessons.

Henry Hazlitt 1948 wrote this in a book “From Bretton Woods to World

Inflation”, which predicted the inevitable collapse of this fixed

exchange rate mechanism. It was a compilation of his editorials from

both his time at the New York Times and Newsweek, which ridiculed the

prevailing economic Keynesian thinking to great effect. A brilliant

journalist, economists and liberal philosopher, this man intuitively

understood the pernicious nature of the Bretton Woods fixed exchange

rate arranged in 1944.

Which made us wonder, just how many countries have engaged in

interventionist currency policy in the last year alone?

Here, for a start, is our preliminary and very non-exhaustive list (in

which we count de facto intervention, suspected intervention and talk

of intervention — and include talk of quantitative easing among the

latter):

•Federal Reserve $ Dollar – via QE.

•Bank of England £ sterling – via QE.

•Japanese yen intervention.

•Taiwan dollar – suspected intervention.

•Argentinian peso intervention.

•Brazil real intervention fears.

•Russian ruble intervention.

•Australian dollar RBA intervention.

•SNB Swiss franc intervention.

•Poland’s NBP zloty intervention.

•Colombia’s peso intervention.

•Indonesian rupiah intervention.

•South Korean won intervention.

•Thai baht intervention fears.

•Ukrainian hryvnia intervention.

•Israeli shekel intervention.

•Chilean peso intervention fears.

•And Turkey has adjusted its reserve requirements in order to weaken the lira.

And also:

•Peruvian sol intervention.

•Phillipines peso suspected intervention.

•Romanian leu intervention.

(From FT's Alphaville)

Within a single week 25 nations have deliberately slashed the values

of their currencies. Nothing quite comparable with this has ever

happened before in the history of the world. This world monetary

earthquake will carry many lessons.

Henry Hazlitt 1948 wrote this in a book “From Bretton Woods to World

Inflation”, which predicted the inevitable collapse of this fixed

exchange rate mechanism. It was a compilation of his editorials from

both his time at the New York Times and Newsweek, which ridiculed the

prevailing economic Keynesian thinking to great effect. A brilliant

journalist, economists and liberal philosopher, this man intuitively

understood the pernicious nature of the Bretton Woods fixed exchange

rate arranged in 1944.

Which made us wonder, just how many countries have engaged in

interventionist currency policy in the last year alone?

Here, for a start, is our preliminary and very non-exhaustive list (in

which we count de facto intervention, suspected intervention and talk

of intervention — and include talk of quantitative easing among the

latter):

•Federal Reserve $ Dollar – via QE.

•Bank of England £ sterling – via QE.

•Japanese yen intervention.

•Taiwan dollar – suspected intervention.

•Argentinian peso intervention.

•Brazil real intervention fears.

•Russian ruble intervention.

•Australian dollar RBA intervention.

•SNB Swiss franc intervention.

•Poland’s NBP zloty intervention.

•Colombia’s peso intervention.

•Indonesian rupiah intervention.

•South Korean won intervention.

•Thai baht intervention fears.

•Ukrainian hryvnia intervention.

•Israeli shekel intervention.

•Chilean peso intervention fears.

•And Turkey has adjusted its reserve requirements in order to weaken the lira.

And also:

•Peruvian sol intervention.

•Phillipines peso suspected intervention.

•Romanian leu intervention.

Tuesday, September 28, 2010

Trial baloons...

...like a hot-air baloon convention in Fed Land...

First, the set up and "intellectual justification" from the San Francisco branch of the Fed:

"Conventional wisdom holds that severe recessions are typically followed by rapid recoveries. But more than a year after the end of the most severe recession since 1947, the recovery is proceeding at a tepid pace. This is happening despite massive federal fiscal stimulus and extremely low interest rates. Forecasts derived from the Chicago and Philadelphia Fed business cycle indicators predict that real GDP growth through the first half of 2011 will remain at or below potential. When translated into a forecast for the labor market, our analysis suggests that the unemployment rate could rise anywhere from 0 to 0.5 percentage point during this period.

A sluggish recovery should perhaps be expected. The recent recession was preceded by a decade-long consumption and housing boom financed by an unsustainable run-up in household debt relative to income (see Lansing 2005). Current efforts to stimulate consumer spending with low interest rates may be less effective than in the past because households remain overleveraged (see Glick and Lansing 2009). In a comprehensive historical review of periods leading up to financial crises and their aftermath, Reinhart and Reinhart (2010) find that episodes of prosperity that are fueled by easy credit and rising debt are typically followed by lengthy periods of deleveraging characterized by subdued growth in GDP and employment.

David Lang is a research associate at the Federal Reserve Bank of San Francisco."

...then pinging the community about the execution of QE:

INSTEAD OF SHOCK AND AWE, is the Federal Reserve preparing surgical strikes to spur the economy?

An article on the Wall Street Journal's Web site late Monday afternoon said the Fed was considering a smaller, open-ended plan to buy Treasury securities, in contrast to the massive, $1.7 trillion securities purchase the central bank undertook beginning in March 2009.

But instead of the Fed setting an amount of securities it would buy, the WSJ.com story by Jon Hilsenrath said the central bank was studying announcing purchases in smaller increments and conditioned on the state of the economy.

It should be recalled that Hilsenrath broke the story during the summer that the Fed would consider replacing maturing mortgage-backed securities rather than letting them run off. As it happened, that approach was approved at the Aug. 10 meeting of the Federal Open Market Committee in order to prevent a passive tightening of monetary policy.

At last week's meeting, the FOMC pointedly said that inflation is currently "somewhat below those the Committee judges most consistent, over the longer run, with its mandate to promote maximum employment and price stability." As a result, the panel added "it is prepared to provide additional accommodation if needed to support the economic recovery and to return inflation, over time, to levels consistent with its mandate."

That statement was widely inferred by market participants that the Fed could take further steps toward "quantitative easing"—the academic term for central bank securities purchases—at the next FOMC meeting on Nov. 2-3 (conveniently concluding the day after Election Day.)

A small-scale approach to purchasing, say, $100 billion or less per month, might bridge disagreements on the FOMC, some of whose members are reluctant to commit to a large-scale QE2 (as a second phase of quantitative easing is being dubbed) at this time.

The trouble...

...with floating exchange rates is that they, like every other operating arm of centralized government, can be utilized for political purposes.

De-valuing the currency via QE (somewhat of a misnomer as I have pointed out in the past, the point being the intent involved) or other monetary mechanism, such as outright foreign currency purchases, amounts to instant global tariffs on imports. This is Monetary Mercantilism and as the below remarks demonstrate, the developed world is indeed mired in the quagmire.

An “international currency war” has broken out, according to Guido Mantega, Brazil’s finance minister, as governments around the globe compete to lower their exchange rates to boost competitiveness.

Mr Mantega’s comments in São Paulo on Monday follow a series of recent interventions by central banks, in Japan, South Korea and Taiwan in an effort to make their currencies cheaper. China, an export powerhouse, has continued to suppress the value of the renminbi, in spite of pressure from the US to allow it to rise, while officials from countries ranging from Singapore to Colombia have issued warnings over the strength of their currencies.

“We’re in the midst of an international currency war, a general weakening of currency. This threatens us because it takes away our competitiveness,” Mr Mantega said. By publicly asserting the existence of a “currency war”, Mr Mantega has admitted what many policymakers have been saying in private: a rising number of countries see a weaker exchange rate as a way to lift their economies.

A weaker exchange rate makes a country’s exports cheaper, potentially boosting a key source of growth for economies battling to find growth as they emerge from the global downturn.

The proliferation of countries trying to manage their exchange rates down is also making it difficult to co-ordinate the issue in global economic forums.

South Korea, the host of the upcoming G20 meeting in November, is reluctant to highlight the issue on the gathering’s agenda, also partly out of fear of offending China, its neighbour and main trading partner.

De-valuing the currency via QE (somewhat of a misnomer as I have pointed out in the past, the point being the intent involved) or other monetary mechanism, such as outright foreign currency purchases, amounts to instant global tariffs on imports. This is Monetary Mercantilism and as the below remarks demonstrate, the developed world is indeed mired in the quagmire.

An “international currency war” has broken out, according to Guido Mantega, Brazil’s finance minister, as governments around the globe compete to lower their exchange rates to boost competitiveness.

Mr Mantega’s comments in São Paulo on Monday follow a series of recent interventions by central banks, in Japan, South Korea and Taiwan in an effort to make their currencies cheaper. China, an export powerhouse, has continued to suppress the value of the renminbi, in spite of pressure from the US to allow it to rise, while officials from countries ranging from Singapore to Colombia have issued warnings over the strength of their currencies.

“We’re in the midst of an international currency war, a general weakening of currency. This threatens us because it takes away our competitiveness,” Mr Mantega said. By publicly asserting the existence of a “currency war”, Mr Mantega has admitted what many policymakers have been saying in private: a rising number of countries see a weaker exchange rate as a way to lift their economies.

A weaker exchange rate makes a country’s exports cheaper, potentially boosting a key source of growth for economies battling to find growth as they emerge from the global downturn.

The proliferation of countries trying to manage their exchange rates down is also making it difficult to co-ordinate the issue in global economic forums.

South Korea, the host of the upcoming G20 meeting in November, is reluctant to highlight the issue on the gathering’s agenda, also partly out of fear of offending China, its neighbour and main trading partner.

Monday, September 27, 2010

Stranger than fiction...

...one of my favorite distractions is "The Onion", an irreverent "newpaper" here in the States. One of my all-time favorite political skits can be found here.

Given my posts on the failed state south of our border, I found this article from the latest Onion most apropos:

MEXICO CITY—In the latest incident of drug-related violence to hit the country, all 111 million citizens of Mexico were killed Monday during a shoot-out between rival drug cartels.

According to the U.S. Drug Enforcement Administration, the violence was sparked by a botched drug deal involving an estimated 20 kilograms of marijuana, a dispute that led low-level members of the Sinaloa cartel to open fire on local dealers in Culiacán. Within seconds, the gunfire had spread to Chihuahua, Michoacán, Yucatán, and, minutes later, the other 27 Mexican states, leaving every person in Mexico dead.

"We're still piecing together details, but it looks as though the incident began as an act of retaliation against Sinaloa by two foot soldiers from the Los Zetas cartel," DEA administrator Michele Leonhart said. "The Gulf and Tijuana cartels then responded before being ambushed by La Familia Michoacána and Los Negros. At that point, witnesses reported hearing roughly 357 million gunshots, during which time the Mexican populace was caught in the crossfire and killed."

"A four-gram bag of cocaine was also recovered by agents," Leonhart added.

Given my posts on the failed state south of our border, I found this article from the latest Onion most apropos:

MEXICO CITY—In the latest incident of drug-related violence to hit the country, all 111 million citizens of Mexico were killed Monday during a shoot-out between rival drug cartels.

According to the U.S. Drug Enforcement Administration, the violence was sparked by a botched drug deal involving an estimated 20 kilograms of marijuana, a dispute that led low-level members of the Sinaloa cartel to open fire on local dealers in Culiacán. Within seconds, the gunfire had spread to Chihuahua, Michoacán, Yucatán, and, minutes later, the other 27 Mexican states, leaving every person in Mexico dead.

"We're still piecing together details, but it looks as though the incident began as an act of retaliation against Sinaloa by two foot soldiers from the Los Zetas cartel," DEA administrator Michele Leonhart said. "The Gulf and Tijuana cartels then responded before being ambushed by La Familia Michoacána and Los Negros. At that point, witnesses reported hearing roughly 357 million gunshots, during which time the Mexican populace was caught in the crossfire and killed."

"A four-gram bag of cocaine was also recovered by agents," Leonhart added.

The Paper Dragon...

...and the "construction boom".

This Link is a hilarious exposition on GDP figure manipulation (assuming China even bothers to properly and sagaciously calculate its own GDP)

This Link is a hilarious exposition on GDP figure manipulation (assuming China even bothers to properly and sagaciously calculate its own GDP)

Uni-directional...

...even the "smallest transfers". I am curious as to how this will collide with a presumed "right" to privacy.

Money transfers face new scrutiny

By Ellen Nakashima Washington Post Staff Writer

Monday, September 27, 2010

The Obama administration wants to require U.S. banks to report all electronic money transfers into and out of the country, a dramatic expansion in efforts to counter terrorist financing and money laundering.

Officials say the information would help them spot the sort of transfers that helped finance the al-Qaeda hijackers who carried out the Sept. 11, 2001, attacks. They say the expanded financial data would allow anti-terrorist agencies to better understand normal money-flow patterns so they can spot abnormal activity.

Financial institutions are now required to report to the Treasury Department transactions in excess of $10,000 and others they deem suspicious. The new rule would require banks to disclose even the smallest transfers.

Treasury officials plan to post the proposed regulation on their Web site Monday and in the Federal Register this week. The public could comment before a final rule is published and the plan takes effect, which officials say will probably not be until 2012.

Money transfers face new scrutiny

By Ellen Nakashima Washington Post Staff Writer

Monday, September 27, 2010

The Obama administration wants to require U.S. banks to report all electronic money transfers into and out of the country, a dramatic expansion in efforts to counter terrorist financing and money laundering.

Officials say the information would help them spot the sort of transfers that helped finance the al-Qaeda hijackers who carried out the Sept. 11, 2001, attacks. They say the expanded financial data would allow anti-terrorist agencies to better understand normal money-flow patterns so they can spot abnormal activity.

Financial institutions are now required to report to the Treasury Department transactions in excess of $10,000 and others they deem suspicious. The new rule would require banks to disclose even the smallest transfers.

Treasury officials plan to post the proposed regulation on their Web site Monday and in the Federal Register this week. The public could comment before a final rule is published and the plan takes effect, which officials say will probably not be until 2012.

Sunday, September 26, 2010

Demand has not fallen...

...and supply remains plentiful. What other choice but to legalize (or at least de-criminalize).

In Law School, the chief of police for the City of Chicago was kind enough to present himself as a guest speaker for one of my classes, the subject being drugs and drug law.

I (just paddling out into the water of economic analysis as applied to legal questions at the time) simply asked him one question:

"Have your interdiction and seizure efforts effected the PRICE of cocaine? In other words, have you seen a measureable and significant increase in the price of cocaine because of the Department's efforts?"

His answer? No price increase. In fact, a large decrease in price and increase in purity was observed. This led me to hold my current view that the "war" on drugs is simply unwinnable...victory is not even a realistic condition in this case. I recognize that this is a difficult issue in that "economic externalities" are a real cost on society, but that is another discussion.

So who has prospered under this war?

The Senate's top Republican on foreign policy said this weekend that drug traffickers operating on the Mexican border pose a more immediate national security threat than domestic terrorists.

Sen. Richard Lugar (Ind.), senior Republican on the Senate Foreign Relations Committee, is calling on the White House to intensify efforts to help Mexico fight drug lords at the border, where escalating violence has killed tens of thousands of people in the past few years.

"Transnational drug trafficking organizations operating from Mexico represent the most immediate national security threat faced by the United States in the Western Hemisphere," Lugar said in remarks prepared for an Indiana-based training for Mexican prosecutors Sunday, Reuters reports.

"The United States should undertake a broad review of further steps the U.S. military and the intelligence community could take to help combat the Mexican cartels in association with the Mexican government."

The Indiana Republican is suggesting the U.S. military and intelligence communities provide Mexico with more surveillance help, to combat the flow of drugs, money and weapons across the 1,969 mile border, Reuters reports.

In Law School, the chief of police for the City of Chicago was kind enough to present himself as a guest speaker for one of my classes, the subject being drugs and drug law.

I (just paddling out into the water of economic analysis as applied to legal questions at the time) simply asked him one question:

"Have your interdiction and seizure efforts effected the PRICE of cocaine? In other words, have you seen a measureable and significant increase in the price of cocaine because of the Department's efforts?"

His answer? No price increase. In fact, a large decrease in price and increase in purity was observed. This led me to hold my current view that the "war" on drugs is simply unwinnable...victory is not even a realistic condition in this case. I recognize that this is a difficult issue in that "economic externalities" are a real cost on society, but that is another discussion.

So who has prospered under this war?

The Senate's top Republican on foreign policy said this weekend that drug traffickers operating on the Mexican border pose a more immediate national security threat than domestic terrorists.

Sen. Richard Lugar (Ind.), senior Republican on the Senate Foreign Relations Committee, is calling on the White House to intensify efforts to help Mexico fight drug lords at the border, where escalating violence has killed tens of thousands of people in the past few years.

"Transnational drug trafficking organizations operating from Mexico represent the most immediate national security threat faced by the United States in the Western Hemisphere," Lugar said in remarks prepared for an Indiana-based training for Mexican prosecutors Sunday, Reuters reports.

"The United States should undertake a broad review of further steps the U.S. military and the intelligence community could take to help combat the Mexican cartels in association with the Mexican government."

The Indiana Republican is suggesting the U.S. military and intelligence communities provide Mexico with more surveillance help, to combat the flow of drugs, money and weapons across the 1,969 mile border, Reuters reports.

Saturday, September 25, 2010

Failed State watch...

...disregarding the questions of just how the cartels have become so well funded as to openly challenge national governments, this situation is becoming terminal with more alacrity than I had expected.

SANTIAGO, Mexico (AP) - Bladimiro Montalvo has one of the most dangerous jobs in this colonial town, and in all of Mexico. He's the mayor.

The soft-spoken 67-year-old teacher distributes school supplies, organizes a job fair and works on improving the library. He also tries to avoid ending up like his predecessor, who authorities say was kidnapped and shot to death last month by his own police officers, linked to the Zetas drug gang.

Three other small-town mayors in northeastern Mexico have been killed in the last month—the latest on Thursday—and at least seven have been killed in border states this year.

Mexican drug cartels have increasingly targeted such officials as they fight the government and each other, seeking control of drug markets and routes to the United States. They use isolated, lightly patrolled towns to hide and to stash kidnap victims, weapons and drugs. They must co-opt or eliminate authority figures like mayors to assert control over both residents and police.

SANTIAGO, Mexico (AP) - Bladimiro Montalvo has one of the most dangerous jobs in this colonial town, and in all of Mexico. He's the mayor.

The soft-spoken 67-year-old teacher distributes school supplies, organizes a job fair and works on improving the library. He also tries to avoid ending up like his predecessor, who authorities say was kidnapped and shot to death last month by his own police officers, linked to the Zetas drug gang.

Three other small-town mayors in northeastern Mexico have been killed in the last month—the latest on Thursday—and at least seven have been killed in border states this year.

Mexican drug cartels have increasingly targeted such officials as they fight the government and each other, seeking control of drug markets and routes to the United States. They use isolated, lightly patrolled towns to hide and to stash kidnap victims, weapons and drugs. They must co-opt or eliminate authority figures like mayors to assert control over both residents and police.

Tuesday, September 21, 2010

Filtering down...

...to the mass media. This is a good article in Forbes of all places.

Here is how to do it better. First of all, forget the dozens of economic statistics, especially the ones published by the U.S. government. Many are “seasonally adjusted,” which simply means they are good for nothing. Then, several months later, they get substantially revised. How can you know what is important and what is not? Here is a guide you should copy and put on your trading computer.

Credit growth: The most important indicator is “credit growth” or lack thereof. Everything else follows. Actually, you could stop right there. However, there are two other factors to assist you, although they depend on credit growth.

Job growth: This is the most important economic factor dependent on credit growth. If there is no credit growth, then there will not be any sustainable job growth.

Consumer spending: For stock investors, the most important indicator is “consumer spending.” Consumer spending is a coincident indicator. When it declines, so does the stock market. It helped us identify the 2007 stock market top. If there is no job growth, then spending will depend on consumers who have jobs spending more. This can happen, but it can’t be sustainable. We have seen this over the past 16 months.

There you have it. Its simple. You can skip all the dozens of other economic numbers if you follow the above. That’s how I knew at the start of this year that the economy would falter. What is the economy doing now?

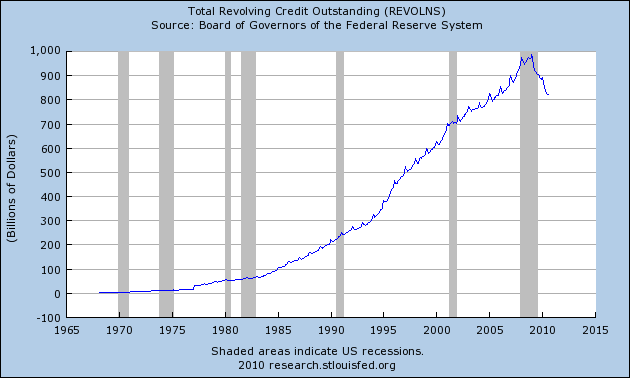

Credit card debt has been declining for 21 months and is now down about $150 billion dollars from its peak. Does anyone really believe that the retail sector can flourish with this shrinkage? Commercial & Industrial loans (to businesses) see no rise at all. There is no credit growth.

The latest job reports have been absolute disasters, confirming my view that the economy is doing very poorly. The theory of the “V-shaped” recovery is now being abandoned by the bulls. They are now changing their tune to “a soft patch” in the economy, just as I predicted. Some economists now mention a “square root-shaped” recovery. Soon, they will start considering a “double dip.” But that will also be the optimistic view. A “dip” infers a slight decline. However, it could be much deeper.

Here is how to do it better. First of all, forget the dozens of economic statistics, especially the ones published by the U.S. government. Many are “seasonally adjusted,” which simply means they are good for nothing. Then, several months later, they get substantially revised. How can you know what is important and what is not? Here is a guide you should copy and put on your trading computer.

Credit growth: The most important indicator is “credit growth” or lack thereof. Everything else follows. Actually, you could stop right there. However, there are two other factors to assist you, although they depend on credit growth.

Job growth: This is the most important economic factor dependent on credit growth. If there is no credit growth, then there will not be any sustainable job growth.

Consumer spending: For stock investors, the most important indicator is “consumer spending.” Consumer spending is a coincident indicator. When it declines, so does the stock market. It helped us identify the 2007 stock market top. If there is no job growth, then spending will depend on consumers who have jobs spending more. This can happen, but it can’t be sustainable. We have seen this over the past 16 months.

There you have it. Its simple. You can skip all the dozens of other economic numbers if you follow the above. That’s how I knew at the start of this year that the economy would falter. What is the economy doing now?

Credit card debt has been declining for 21 months and is now down about $150 billion dollars from its peak. Does anyone really believe that the retail sector can flourish with this shrinkage? Commercial & Industrial loans (to businesses) see no rise at all. There is no credit growth.

The latest job reports have been absolute disasters, confirming my view that the economy is doing very poorly. The theory of the “V-shaped” recovery is now being abandoned by the bulls. They are now changing their tune to “a soft patch” in the economy, just as I predicted. Some economists now mention a “square root-shaped” recovery. Soon, they will start considering a “double dip.” But that will also be the optimistic view. A “dip” infers a slight decline. However, it could be much deeper.

Manacles...

...were emplaced by the framers for very, very good reasons. I have no objection to updating machanisms that apply the constitution to "ever-changing circumstances", but to say that "history is uncertain" vis a vis the uncertainty of subjective argument is disengenous. This is about power, not the ability to apply some pricipal that is the most asymptotic to some definition of the constitution's "purpose".

Breyer's new book, "Making Our Democracy Work," underlines their disagreement in a chapter called "The Basic Approach."

"The court should reject approaches to interpreting the Constitution that consider the document's scope and application as fixed at the moment of framing," Breyer writes. "Rather, the court should regard the Constitution as containing unwavering values that must be applied flexibly to ever-changing circumstances."

Judges should go about this, Breyer says, using "traditional legal tools, such as text, history, tradition, precedent, and purposes and related consequences, to help find proper legal answers. But courts should emphasize certain of these tools, particularly purposes and consequences. Doing so will make the law work better for those whom it affects."

Breyer, 72, said in an interview that he understands how that opens him to criticism of subjectivity, and that his approach lacks the simple message of originalism.

"I've said many times: I can understand why you'd want . . . a simple, clear theory, as if you had a historical computer and could in fact decide on the basis of history the answer to these questions," Breyer said. "But history is too uncertain."

Breyer's new book, "Making Our Democracy Work," underlines their disagreement in a chapter called "The Basic Approach."

"The court should reject approaches to interpreting the Constitution that consider the document's scope and application as fixed at the moment of framing," Breyer writes. "Rather, the court should regard the Constitution as containing unwavering values that must be applied flexibly to ever-changing circumstances."

Judges should go about this, Breyer says, using "traditional legal tools, such as text, history, tradition, precedent, and purposes and related consequences, to help find proper legal answers. But courts should emphasize certain of these tools, particularly purposes and consequences. Doing so will make the law work better for those whom it affects."

Breyer, 72, said in an interview that he understands how that opens him to criticism of subjectivity, and that his approach lacks the simple message of originalism.

"I've said many times: I can understand why you'd want . . . a simple, clear theory, as if you had a historical computer and could in fact decide on the basis of history the answer to these questions," Breyer said. "But history is too uncertain."

Monday, September 20, 2010

Everyone...

...pensions in the U.S. in similar positions. I have stated here before that ZIRP is DEFLATIONARY is this type of recession.

"We are all in the same position," he added. "Every month we make our

funding ratio public and a lot of participants are getting worried

about (their) pensions."

As a result, pensioners have generally seen a freeze in pension

indexation, while employees have seen an increase in their premiums.

"Everyone feels it," said Steger.

ABP reported a funding level of 88% at the end of August; PFZW, 94%;

PMT, 85.2%; bpf, 97.1% and PME, 91%.

Dutch pension regulations require schemes to be 105% funded. To get

back to full funding, pension funds can either freeze the level of

pension payments, increase the premiums paid by employees or cut

benefits. Steger said cutting benefits is always considered a last

resort.

"We are all in the same position," he added. "Every month we make our

funding ratio public and a lot of participants are getting worried

about (their) pensions."

As a result, pensioners have generally seen a freeze in pension

indexation, while employees have seen an increase in their premiums.

"Everyone feels it," said Steger.

ABP reported a funding level of 88% at the end of August; PFZW, 94%;

PMT, 85.2%; bpf, 97.1% and PME, 91%.

Dutch pension regulations require schemes to be 105% funded. To get

back to full funding, pension funds can either freeze the level of

pension payments, increase the premiums paid by employees or cut

benefits. Steger said cutting benefits is always considered a last

resort.

Global competitiveness...

From a report by the Global Economic Forum. Many numbers that preserve the status quo.

Switzerland 1 5.63

Sweden 2 5.56

Singapore 3 5.48

United States 4 5.43

Germany 5 5.39

Japan 6 5.37

Finland 7 5.37

Netherlands 8 5.33

Denmark 9 5.32

Canada 10 5.30

Hong Kong SAR 11 5.27

United Kingdom 12 5.25

Taiwan, China 13 5.21

Norway 14 5.14

France 15 5.13

Australia 16 5.11

Qatar 17 5.10

Austria 18 5.09

Belgium 19 5.07

Luxembourg 20 5.05

Saudi Arabia 21 4.95

Korea, Rep. 22 4.93

Switzerland 1 5.63

Sweden 2 5.56

Singapore 3 5.48

United States 4 5.43

Germany 5 5.39

Japan 6 5.37

Finland 7 5.37

Netherlands 8 5.33

Denmark 9 5.32

Canada 10 5.30

Hong Kong SAR 11 5.27

United Kingdom 12 5.25

Taiwan, China 13 5.21

Norway 14 5.14

France 15 5.13

Australia 16 5.11

Qatar 17 5.10

Austria 18 5.09

Belgium 19 5.07

Luxembourg 20 5.05

Saudi Arabia 21 4.95

Korea, Rep. 22 4.93

Pings...

...from a variety of sources about the continuing problems of "united" Europe. The greatest evils the world has ever seen derive from individuals convincing majorities that the world can be fabricated, hammered, and shoehorned into some normative system. Compare and contrast these systems with the founding of the United States (relative to what it appears to be at the present).

Anyway, the men of Newport Beach have sounded the bell, and now all eyes are focused on Europe's slow motion crash.

The brutal truth is that Portugal lost competitiveness on a grand scale on joining EMU and has never been able to get it back. Convergence never came.

Ireland has shown what happens when you grasp the fiscal nettle, slashing public wages by 13pc – to applause from EU elites – without offsetting monetary and exchange stimulus. Irish bonds have spiked even higher to a post-EMU record 6.38pc.

This was triggered by two client notes: Barclays said Ireland may need the IMF's help; Citigroup's Willem Buiter said Ireland "may not be able to make whole" creditors of both sovereign debt and the bank. Dr Buiter has also said a default by Greece is "a high probability event".

Two years into its purge, Ireland has a budget deficit near 20pc of GDP. It is 12pc if you strip out the bank rescues, but the reason why the bad debts of Anglo Irish keep spiralling upwards is that the economy keeps spiralling downwards. House prices have fallen 35pc. Nominal GDP has contracted 19pc.

"Ireland's debt is ballooning, while its capacity to pay has collapsed," said Simon Johnson, ex-chief economist at the IMF. He said the country has made a Faustian pact with Europe, able to draw ECB loans worth 75pc of GDP so long as Irish taxpayers shield European creditors.

In any case, the IMF itself has become the problem, operating as an arm of EU ideology under Dominique Strauss-Kahn. It

Anyway, the men of Newport Beach have sounded the bell, and now all eyes are focused on Europe's slow motion crash.

The brutal truth is that Portugal lost competitiveness on a grand scale on joining EMU and has never been able to get it back. Convergence never came.

Ireland has shown what happens when you grasp the fiscal nettle, slashing public wages by 13pc – to applause from EU elites – without offsetting monetary and exchange stimulus. Irish bonds have spiked even higher to a post-EMU record 6.38pc.

This was triggered by two client notes: Barclays said Ireland may need the IMF's help; Citigroup's Willem Buiter said Ireland "may not be able to make whole" creditors of both sovereign debt and the bank. Dr Buiter has also said a default by Greece is "a high probability event".

Two years into its purge, Ireland has a budget deficit near 20pc of GDP. It is 12pc if you strip out the bank rescues, but the reason why the bad debts of Anglo Irish keep spiralling upwards is that the economy keeps spiralling downwards. House prices have fallen 35pc. Nominal GDP has contracted 19pc.

"Ireland's debt is ballooning, while its capacity to pay has collapsed," said Simon Johnson, ex-chief economist at the IMF. He said the country has made a Faustian pact with Europe, able to draw ECB loans worth 75pc of GDP so long as Irish taxpayers shield European creditors.

In any case, the IMF itself has become the problem, operating as an arm of EU ideology under Dominique Strauss-Kahn. It

Friday, September 17, 2010

Growth (?)

From the Flow of Funds Accounts for the United States:

"Household net worth—the difference between

the value of assets and liabilities—was an estimated

$53.5 trillion at the end of the second quarter, down

$1.5 trillion from the end of the previous quarter."

"Household net worth—the difference between

the value of assets and liabilities—was an estimated

$53.5 trillion at the end of the second quarter, down

$1.5 trillion from the end of the previous quarter."

1.23 Trillion in Stimulus Spending...

...and no inflation. Zero Interest Rate Policy in effect. No inflation. Once again, preservation of the proper methods is pursued in the face of common sense and to the detriment of the Global Economy.

From the New York Times:

Consumer prices remained mostly flat in August, according to a government report released Friday, another sign that inflation is so tame that the economy could be on the brink of deflation.

Just days ahead of a Federal Reserve policy meeting, the Labor Department said the Consumer Price Index, a benchmark measure of inflation, rose 0.3 percent in August, compared with 0.3 percent in July, on a seasonally adjusted basis. Excluding volatile energy and food prices, the core index was flat in August. It had risen 0.1 percent in July, and 0.2 percent in June.

From the New York Times:

Consumer prices remained mostly flat in August, according to a government report released Friday, another sign that inflation is so tame that the economy could be on the brink of deflation.

Just days ahead of a Federal Reserve policy meeting, the Labor Department said the Consumer Price Index, a benchmark measure of inflation, rose 0.3 percent in August, compared with 0.3 percent in July, on a seasonally adjusted basis. Excluding volatile energy and food prices, the core index was flat in August. It had risen 0.1 percent in July, and 0.2 percent in June.

In the context of the immediately precedeing post...

...please read the following forward from a Brooking's institution book entitled "Greenhouse Governance"

Public deliberation over climate change has traditionally been dominated by the natural and physical sciences. Is the planet warming? To what degree, and is mankind responsible? How big a problem is this, really? But concurrent with these debates is the question of what should be done. Indeed, what can be done? Issues of governance, including the political feasibility of certain policies and their capacity for implementation, have received short shrift in the conversation. But they absolutely must be addressed as we respond to this unprecedented challenge. Greenhouse Governance brings a much-needed public policy mindset to discussion of climate change in America.

Greenhouse Governance features a number of America's preeminent public policy scholars, examining some aspect of governance and climate change. They analyze the state and influence of American public opinion on climate change as well as federalism and intergovernmental relations, which prove especially important since state and local governments have taken a more active role than originally expected. Specific policy issues examined include renewable electricity standards, mandating greater vehicle fuel economy, the "adaptation vs. mitigation" debate, emissions trading, and carbon taxes.

The contributors do consider the scientific and economic questions of climate policy but place special emphasis on political and managerial issues. They analyze the role of key American government institutions including the courts, Congress, and regulatory agencies. The final two chapters put the discussion into an international context, looking at climate governance challenges in North America, relations with the European Union, and possible models for international governance.

Public deliberation over climate change has traditionally been dominated by the natural and physical sciences. Is the planet warming? To what degree, and is mankind responsible? How big a problem is this, really? But concurrent with these debates is the question of what should be done. Indeed, what can be done? Issues of governance, including the political feasibility of certain policies and their capacity for implementation, have received short shrift in the conversation. But they absolutely must be addressed as we respond to this unprecedented challenge. Greenhouse Governance brings a much-needed public policy mindset to discussion of climate change in America.

Greenhouse Governance features a number of America's preeminent public policy scholars, examining some aspect of governance and climate change. They analyze the state and influence of American public opinion on climate change as well as federalism and intergovernmental relations, which prove especially important since state and local governments have taken a more active role than originally expected. Specific policy issues examined include renewable electricity standards, mandating greater vehicle fuel economy, the "adaptation vs. mitigation" debate, emissions trading, and carbon taxes.

The contributors do consider the scientific and economic questions of climate policy but place special emphasis on political and managerial issues. They analyze the role of key American government institutions including the courts, Congress, and regulatory agencies. The final two chapters put the discussion into an international context, looking at climate governance challenges in North America, relations with the European Union, and possible models for international governance.

Thursday, September 16, 2010

Operating Systems

Much of "civilization" as we know consists of the promulgation of ideas that either convince or coerce an individual to disregard his/her self interest for the betterment of another individual or group of individuals. These "operating systems" instill perspectives amongst its adherants, be it concepts of "fairness", "freedom", "natural law", etc. Once these ideas are firmly enconced, the burden of proof lies with any competing system of thought (hence the constant reinforcement, by propaganda and other methods, of these central ideas), and any countervailing operating system is viewed as a malignant virus.

It is interesting to note that in the current secular age, government, and more specifically "rights" imbued by documents have supplanted Religion as the "operating system" of choice throghout the civilized world. And, the patterns that we observed throughout history concerning Religious operating systems have clearly been replicated in the current age.

I am speaking specifically about the tendency of power to concentrate.

I believe that market driven solutions are superior to any alternatives. This is because market driven solutions allocate resources efficiently and without regard to competing operating systems that exist to subordinate individual self-interest.

Once self-interest is encroached upon, the precedent has been set for the gradual, irreversable descent into servitude. This effect scales massively; the more subjects who subscribe to a given operating system, the more power will ascend to the top echelon of of system admins and programmers. Extreme examples of this are religious cults, who blindly trust their leaders to the death.

So, ask yourself a question: are you behaving in your own interest or at the behest of others you have never met? Who benefits from this set of circumstance?

Wednesday, September 15, 2010

QE2

Since there will be more manifestations of QE, and certainly more beyond QE2 as the Government (The Fed, the Treasury, the Executive, and Congress) continues to fire blanks at a charging 2000lb. bull, but cannot de-ossify themselves from traditional Keynesian stimulus packages, here are my nominees for the putative rounds of QE:

QE3: "Beyond the Valley of Quantitative Easement"

QE4: "Return of QE"

QE5: "Revenge of QE"

QE6: "The FINAL chapter of QE"

QE7: "Son of QE"

QE8: "Greenspan's Vengeful Ghost"

QE9: "QEen of the Damned"

QE10: "QE X"

...and on and on until someone realizes (as per the previous post) that there must be a better way to increase aggregate demand...that way being of course tax cuts to build demand from the bottom up and CHANGE consumer preferences on a more permanent basis, something QE is powerless to do.

Charge of the Fed Brigade...

'Forward, the Fed Brigade!'

Was there a Economist dismay'd ?

Not tho' the beaurocrat knew

Some one had blunder'd:

Theirs not to make reply,

Theirs not to reason why,

Theirs but to do & die,

Into the valley of Stimulus

Rode the PhDs...

QE2, ZIRP, calls for more stimulus, and yet we still have academic papers and official white papers published explaining why these measures work and tax cuts do not. Never mind that the reason d'etre of the academic economics profession is distributing power among policy makers to perform these measures.

It is axiomatic that those who hold power use traditional mechanisms in their decision making processes...otherwise there woudl be no need for them. The British military suffered a similar eureka moment when they realized that officer commissions should be based on merit as opposed to geneology. The light brigade was one of those moments when someone with influence says "there must be a better way".

Tuesday, September 14, 2010

Expropriation risk...

...Once again, property guarantees without corresponding security guarantees are only worth the time value between elections/uprisings/revolutions/coups/etc.

The U.S. has an incredible advantage vis a vis the rest of the world (especially China, the U.S. has much experience in destabilizing Communist economies in emerging countries...)

"There are many foreigners who don’t buy to produce, but rather to position themselves in places with water, mineral resources and hydrocarbons," said Pablo Orsolini, a sponsor of the legislation.

In Madasgascar, a deal with Korea's Daiwoo Logistics to plant corn on territory half the size of Belgium led to the downfall of the government in 2008. The lease was revoked. "Madagascar's land is neither for sale nor for rent," said the new president. Even Australia's senate has called for an audit of foreign-owned land and water projects.

The allure of global land is obvious. The World Bank says industrial and “transition” countries are losing 2.9m hectares of cultivated farmland each year. China is paving over its fertile belt on the Eastern seabord, and depleting the water basin of the North China Plain for crop irrigation.

Cheng Siwei, head of China's green energy drive, told me last week that eco-damage of 13.5pc of GDP each year outstrips China’s growth rate of 10pc. National wealth is contracting. "We have an intangible environmental debt that we are leaving to our children," he said. So does India. Much of the globe is stealing food from the future.

The U.S. has an incredible advantage vis a vis the rest of the world (especially China, the U.S. has much experience in destabilizing Communist economies in emerging countries...)

"There are many foreigners who don’t buy to produce, but rather to position themselves in places with water, mineral resources and hydrocarbons," said Pablo Orsolini, a sponsor of the legislation.

In Madasgascar, a deal with Korea's Daiwoo Logistics to plant corn on territory half the size of Belgium led to the downfall of the government in 2008. The lease was revoked. "Madagascar's land is neither for sale nor for rent," said the new president. Even Australia's senate has called for an audit of foreign-owned land and water projects.

The allure of global land is obvious. The World Bank says industrial and “transition” countries are losing 2.9m hectares of cultivated farmland each year. China is paving over its fertile belt on the Eastern seabord, and depleting the water basin of the North China Plain for crop irrigation.

Cheng Siwei, head of China's green energy drive, told me last week that eco-damage of 13.5pc of GDP each year outstrips China’s growth rate of 10pc. National wealth is contracting. "We have an intangible environmental debt that we are leaving to our children," he said. So does India. Much of the globe is stealing food from the future.

When the chips come down...

...who will Japan side with?

In its annual white paper released Friday, the Defense Ministry expressed concern about recent Chinese navy activities in waters around Japan.

The report, the first under the Democratic Party of Japan administration, detailed specific drills and activities in its assessment of Chinese naval power.

The document was originally slated for release in late July.

It was postponed over concern that its mention of islets claimed by both Tokyo and Seoul could rekindle anti-Japanese sentiment in South Korea prior to the Aug. 29 centenary of Japan's colonization of the Korean Peninsula.

But as in past reports, it described the Takeshima islets (Dokdo in Korean) as an "integral part" of Japanese territory.

On China, it said uncertainties about the country's defense policy and military strength are a matter of concern to the region, including Japan, and the international community.

It went on to describe in detail such incidents as a fleet of Chinese warships, including submarines, passing in waters between Okinawan islands during a drill and a Chinese navy helicopter buzzing vessels of the Self-Defense Forces in April.

In its annual white paper released Friday, the Defense Ministry expressed concern about recent Chinese navy activities in waters around Japan.

The report, the first under the Democratic Party of Japan administration, detailed specific drills and activities in its assessment of Chinese naval power.

The document was originally slated for release in late July.

It was postponed over concern that its mention of islets claimed by both Tokyo and Seoul could rekindle anti-Japanese sentiment in South Korea prior to the Aug. 29 centenary of Japan's colonization of the Korean Peninsula.

But as in past reports, it described the Takeshima islets (Dokdo in Korean) as an "integral part" of Japanese territory.

On China, it said uncertainties about the country's defense policy and military strength are a matter of concern to the region, including Japan, and the international community.

It went on to describe in detail such incidents as a fleet of Chinese warships, including submarines, passing in waters between Okinawan islands during a drill and a Chinese navy helicopter buzzing vessels of the Self-Defense Forces in April.

Mexico...

As I have said here many times. This is a failed state.

WASHINGTON—The Obama administration sees the drug-related violence sweeping Mexico as a growing threat to U.S. national security and has launched a broad review of steps the military and intelligence community could take to help combat what some U.S. officials describe as a narcoinsurgency.

U.S. and Mexican officials say the Pentagon's Northern Command, the Department of Homeland Security and other agencies are discussing what aviation, surveillance and intelligence assets could be used—both inside Mexico and along the border—to help counter the drug cartels.

WASHINGTON—The Obama administration sees the drug-related violence sweeping Mexico as a growing threat to U.S. national security and has launched a broad review of steps the military and intelligence community could take to help combat what some U.S. officials describe as a narcoinsurgency.

U.S. and Mexican officials say the Pentagon's Northern Command, the Department of Homeland Security and other agencies are discussing what aviation, surveillance and intelligence assets could be used—both inside Mexico and along the border—to help counter the drug cartels.

Guarantees...

When the Fed ostensibly guarantees a positive risk-free return, such a deal is difficult to turn down, which is precisely what is happening with money-center banks and the Treausry curve. Free financing for a positive return, and precious few prospects for continued lending given aggregate demand...and the political administration wonders why their calls to action on credit leniancy fall on deaf ears...

Access to Treasury bond auctions is now a massive competitive advantage to the money center banks, and bond auctions will go very well until this imbalance is corrected.

Access to Treasury bond auctions is now a massive competitive advantage to the money center banks, and bond auctions will go very well until this imbalance is corrected.

That squeezing sound...

...you hear is from middle market firms being impacted by bank policies (which I will address in the next post).

Long term vs. Short term

Mean reversion is a simple concept, and yet the human psyche seems ill-equipped to address the consequences of statistical near-certainty.

There is a very good reason why 1-3-5 year returns are the industry standard; these relatively short time periods correspond nicely with Man's ability comprehend the future in reference to his past.

Tuesday, September 07, 2010

Disingenuous

My comments are in italics. This is bad comedy.

By PAUL KRUGMAN

Published: September 5, 2010

Here’s the situation: The U.S. economy has been crippled by a

financial crisis. The president’s policies have limited the damage,

but they were too cautious, and unemployment remains disastrously

high. More action is clearly needed. Yet the public has soured on

government activism, and seems poised to deal Democrats a severe

defeat in the midterm elections.

The policies have not limited the damage. The 1.2 Trillion in "Stimulus" and directed ZIRP policy to the Fed was not cautious. I agree the public has soured on the government's actions, and rightly so.

The president in question is Franklin Delano Roosevelt; the year is

1938. Within a few years, of course, the Great Depression was over.

But it’s both instructive and discouraging to look at the state of

America circa 1938 — instructive because the nature of the recovery

that followed refutes the arguments dominating today’s public debate, discouraging because it’s hard to see anything like the miracle of the 1940s happening again.

Ah, very good, a historical curve ball. But do the events that dominate the 1940s qualify as a "miracle" in the Theological sense of the word?

Now, we weren’t supposed to find ourselves replaying the late 1930s.

President Obama’s economists promised not to repeat the mistakes of

1937, when F.D.R. pulled back fiscal stimulus too soon. But by making his program too small and too short-lived, Mr. Obama did just that: the stimulus raised growth while it lasted, but it made only a small dent in unemployment — and now it’s fading out.

There were "significant events" during FDR's administration (covered below) that made "fiscal stimulus" a necessity.

And just as some of us feared, the inadequacy of the administration’s initial economic plan has landed it — and the nation — in a political trap. More stimulus is desperately needed, but in the public’s eyes the failure of the initial program to deliver a convincing recovery has discredited government action to create jobs.

What causality are we talking about? The public's perception leads to job creation by fiscal stimulus? The public would not presumably be against large tax cuts that would stimulate the economy grom the bottom up.

In short, welcome to 1938.

The story of 1937, of F.D.R.’s disastrous decision to heed those who

said that it was time to slash the deficit, is well known. What’s less well known is the extent to which the public drew the wrong

conclusions from the recession that followed: far from calling for a

resumption of New Deal programs, voters lost faith in fiscal

expansion.

The Kyhber Pass approach to economic policy. Perhaps the public's rejection of New Deal programs was because top-down stimulus efforts are far, far less efficient than bottom up Fiscal Stimulus via tax cuts, putting more funds in the pockets of individuals to choose where to properly allocate resources via price mechanisms.

Consider Gallup polling from March 1938. Asked whether government

spending should be increased to fight the slump, 63 percent of those

polled said no. Asked whether it would be better to increase spending or to cut business taxes, only 15 percent favored spending; 63 percent favored tax cuts. And the 1938 election was a disaster for the Democrats, who lost 70 seats in the House and seven in the Senate.

My goodness...what will the unwashed masses think of next?

Then came the war.

From an economic point of view World War II was, above all, a burst of deficit-financed government spending, on a scale that would never have been approved otherwise. Over the course of the war the federal government borrowed an amount equal to roughly twice the value of G.D.P. in 1940 — the equivalent of roughly $30 trillion today.

I am speechless. If only we had an immense war, public opinion regarding fiscal stimulus would shift towards enormous government spending, and that is the best policy?

Had anyone proposed spending even a fraction that much before the war, people would have said the same things they’re saying today. They would have warned about crushing debt and runaway inflation. They would also have said, rightly, that the Depression was in large part caused by excess debt — and then have declared that it was impossible to fix this problem by issuing even more debt.

Once again, if only the unwashed masses could understand that Government should be given carte blanche to spend and do as it wishes without compunction, check, or limitation.

But guess what? Deficit spending created an economic boom — and the

boom laid the foundation for long-run prosperity. Overall debt in the economy — public plus private — actually fell as a percentage of

G.D.P., thanks to economic growth and, yes, some inflation, which

reduced the real value of outstanding debts. And after the war, thanks to the improved financial position of the private sector, the economy was able to thrive without continuing deficits.

Yay war!

The economic moral is clear: when the economy is deeply depressed, the usual rules don’t apply. Austerity is self-defeating: when everyone tries to pay down debt at the same time, the result is depression and deflation, and debt problems grow even worse. And conversely, it is possible — indeed, necessary — for the nation as a whole to spend its way out of debt: a temporary surge of deficit spending, on a sufficient scale, can cure problems brought on by past excesses.

Ah, the real reason for this article. This is no different from Hegal and Machiavelli genuflecting and legitimizing the actions of Frederich Willliam III and King Ferdinand, respectively. This article is an advertisement for top-down deficit spending, the preferred method of Fiscal stimulus as Government holds the purse strings. Tax cuts and mortgage forgiveness would be much better policy options to combat austerity, but have the unfortunate property of rendering Government action moot.

But the story of 1938 also shows how hard it is to apply these

insights. Even under F.D.R., there was never the political will to do what was needed to end the Great Depression; its eventual resolution came essentially by accident.

The unwashed massed are wrong, the cloistered elite are right. Arrogance.

I had hoped that we would do better this time. But it turns out that

politicians and economists alike have spent decades unlearning the

lessons of the 1930s, and are determined to repeat all the old

mistakes. And it’s slightly sickening to realize that the big winners in the midterm elections are likely to be the very people who first got us into this mess, then did everything in their power to block action to get us out.

Then write a book, run for election, declare yourself chancellor, and start a war! Just ignore those pesky plebians who lack the "triumphant will" to do what is necessary.

But always remember: this slump can be cured. All it will take is a

little bit of intellectual clarity, and a lot of political will.

Here’s hoping we find those virtues in the not too distant future.

Enough.

(ADDENDUM) The Deficit spending during WWII that created the Krugman "miracle" had the advantagous condition of an untouched supplier of post-war industrial and consumer goods (the U.S.) coupled with large swathes of populations that required these goods (The rest of the developed world). Where is this corresponding relationship in Krugman's analysis?

By PAUL KRUGMAN

Published: September 5, 2010

Here’s the situation: The U.S. economy has been crippled by a

financial crisis. The president’s policies have limited the damage,

but they were too cautious, and unemployment remains disastrously

high. More action is clearly needed. Yet the public has soured on

government activism, and seems poised to deal Democrats a severe

defeat in the midterm elections.

The policies have not limited the damage. The 1.2 Trillion in "Stimulus" and directed ZIRP policy to the Fed was not cautious. I agree the public has soured on the government's actions, and rightly so.

The president in question is Franklin Delano Roosevelt; the year is

1938. Within a few years, of course, the Great Depression was over.

But it’s both instructive and discouraging to look at the state of

America circa 1938 — instructive because the nature of the recovery

that followed refutes the arguments dominating today’s public debate, discouraging because it’s hard to see anything like the miracle of the 1940s happening again.

Ah, very good, a historical curve ball. But do the events that dominate the 1940s qualify as a "miracle" in the Theological sense of the word?

Now, we weren’t supposed to find ourselves replaying the late 1930s.

President Obama’s economists promised not to repeat the mistakes of

1937, when F.D.R. pulled back fiscal stimulus too soon. But by making his program too small and too short-lived, Mr. Obama did just that: the stimulus raised growth while it lasted, but it made only a small dent in unemployment — and now it’s fading out.

There were "significant events" during FDR's administration (covered below) that made "fiscal stimulus" a necessity.

And just as some of us feared, the inadequacy of the administration’s initial economic plan has landed it — and the nation — in a political trap. More stimulus is desperately needed, but in the public’s eyes the failure of the initial program to deliver a convincing recovery has discredited government action to create jobs.

What causality are we talking about? The public's perception leads to job creation by fiscal stimulus? The public would not presumably be against large tax cuts that would stimulate the economy grom the bottom up.

In short, welcome to 1938.

The story of 1937, of F.D.R.’s disastrous decision to heed those who

said that it was time to slash the deficit, is well known. What’s less well known is the extent to which the public drew the wrong

conclusions from the recession that followed: far from calling for a

resumption of New Deal programs, voters lost faith in fiscal

expansion.

The Kyhber Pass approach to economic policy. Perhaps the public's rejection of New Deal programs was because top-down stimulus efforts are far, far less efficient than bottom up Fiscal Stimulus via tax cuts, putting more funds in the pockets of individuals to choose where to properly allocate resources via price mechanisms.

Consider Gallup polling from March 1938. Asked whether government

spending should be increased to fight the slump, 63 percent of those

polled said no. Asked whether it would be better to increase spending or to cut business taxes, only 15 percent favored spending; 63 percent favored tax cuts. And the 1938 election was a disaster for the Democrats, who lost 70 seats in the House and seven in the Senate.

My goodness...what will the unwashed masses think of next?

Then came the war.

From an economic point of view World War II was, above all, a burst of deficit-financed government spending, on a scale that would never have been approved otherwise. Over the course of the war the federal government borrowed an amount equal to roughly twice the value of G.D.P. in 1940 — the equivalent of roughly $30 trillion today.

I am speechless. If only we had an immense war, public opinion regarding fiscal stimulus would shift towards enormous government spending, and that is the best policy?

Had anyone proposed spending even a fraction that much before the war, people would have said the same things they’re saying today. They would have warned about crushing debt and runaway inflation. They would also have said, rightly, that the Depression was in large part caused by excess debt — and then have declared that it was impossible to fix this problem by issuing even more debt.

Once again, if only the unwashed masses could understand that Government should be given carte blanche to spend and do as it wishes without compunction, check, or limitation.

But guess what? Deficit spending created an economic boom — and the

boom laid the foundation for long-run prosperity. Overall debt in the economy — public plus private — actually fell as a percentage of

G.D.P., thanks to economic growth and, yes, some inflation, which

reduced the real value of outstanding debts. And after the war, thanks to the improved financial position of the private sector, the economy was able to thrive without continuing deficits.

Yay war!

The economic moral is clear: when the economy is deeply depressed, the usual rules don’t apply. Austerity is self-defeating: when everyone tries to pay down debt at the same time, the result is depression and deflation, and debt problems grow even worse. And conversely, it is possible — indeed, necessary — for the nation as a whole to spend its way out of debt: a temporary surge of deficit spending, on a sufficient scale, can cure problems brought on by past excesses.

Ah, the real reason for this article. This is no different from Hegal and Machiavelli genuflecting and legitimizing the actions of Frederich Willliam III and King Ferdinand, respectively. This article is an advertisement for top-down deficit spending, the preferred method of Fiscal stimulus as Government holds the purse strings. Tax cuts and mortgage forgiveness would be much better policy options to combat austerity, but have the unfortunate property of rendering Government action moot.

But the story of 1938 also shows how hard it is to apply these

insights. Even under F.D.R., there was never the political will to do what was needed to end the Great Depression; its eventual resolution came essentially by accident.

The unwashed massed are wrong, the cloistered elite are right. Arrogance.

I had hoped that we would do better this time. But it turns out that

politicians and economists alike have spent decades unlearning the

lessons of the 1930s, and are determined to repeat all the old

mistakes. And it’s slightly sickening to realize that the big winners in the midterm elections are likely to be the very people who first got us into this mess, then did everything in their power to block action to get us out.

Then write a book, run for election, declare yourself chancellor, and start a war! Just ignore those pesky plebians who lack the "triumphant will" to do what is necessary.

But always remember: this slump can be cured. All it will take is a

little bit of intellectual clarity, and a lot of political will.

Here’s hoping we find those virtues in the not too distant future.

Enough.

(ADDENDUM) The Deficit spending during WWII that created the Krugman "miracle" had the advantagous condition of an untouched supplier of post-war industrial and consumer goods (the U.S.) coupled with large swathes of populations that required these goods (The rest of the developed world). Where is this corresponding relationship in Krugman's analysis?

Saturday, September 04, 2010

Retroactive Elasticity (a continuing series)

A truly amazing paragraph authroed by Robert Rubin found in a Wall Street Journal article:

From "Bring Back the Estate Tax Now"

Ordinarily in tax matters, the effective date would not precede the

date of enactment, or at least the date that a measure was introduced, because Congress knows that taxpayers make their plans based on the existing code. But in the case of the estate tax, presumably nobody's demise was affected in timing by the structuring of our tax laws. And importantly there has been notice—through the president's budget and statements by public officials—that a tax would be enacted earlier this year that would apply to the whole of this year.

"Notice" and "statements" by public officials are enough to legitimize a retroactive tax?

I disagree. This would usher in a very slippery slope concerning which "statements" could usher in new taxation (and other legislation) retroactively. Furthermore, what "statements" (and by whom) effectively satisfy this "notice" standard that Mr. Rubin has put forth?

In addition, Mr. Rubin ascribes a "planning" component that serves as the main obstacle for establishing a retroactive tax, as if to say that the ability of the taxpayer to "plan" paying his/her taxes serves as the only obstacle in legislating retroactive obligations. But the real economic loss of paying taxes is not merely offset by the ability to "plan" for them. This is bad policy.

From "Bring Back the Estate Tax Now"

Ordinarily in tax matters, the effective date would not precede the

date of enactment, or at least the date that a measure was introduced, because Congress knows that taxpayers make their plans based on the existing code. But in the case of the estate tax, presumably nobody's demise was affected in timing by the structuring of our tax laws. And importantly there has been notice—through the president's budget and statements by public officials—that a tax would be enacted earlier this year that would apply to the whole of this year.

"Notice" and "statements" by public officials are enough to legitimize a retroactive tax?

I disagree. This would usher in a very slippery slope concerning which "statements" could usher in new taxation (and other legislation) retroactively. Furthermore, what "statements" (and by whom) effectively satisfy this "notice" standard that Mr. Rubin has put forth?

In addition, Mr. Rubin ascribes a "planning" component that serves as the main obstacle for establishing a retroactive tax, as if to say that the ability of the taxpayer to "plan" paying his/her taxes serves as the only obstacle in legislating retroactive obligations. But the real economic loss of paying taxes is not merely offset by the ability to "plan" for them. This is bad policy.

Retroactive elasticity

The following paragraph, taken from a book about economics I am currently reading, illustrates one of the major fallacies replete within economic thinking; selective behavior bias of homo econimus.